Venture debt is essentially a high-interest loan advanced to early stage companies that want to raise capital without diluting equity, or one that they turn to when venture capital becomes scarce. To be sure, although venture debt has gained significant ground, venture capital remains the main source of finance for startups.

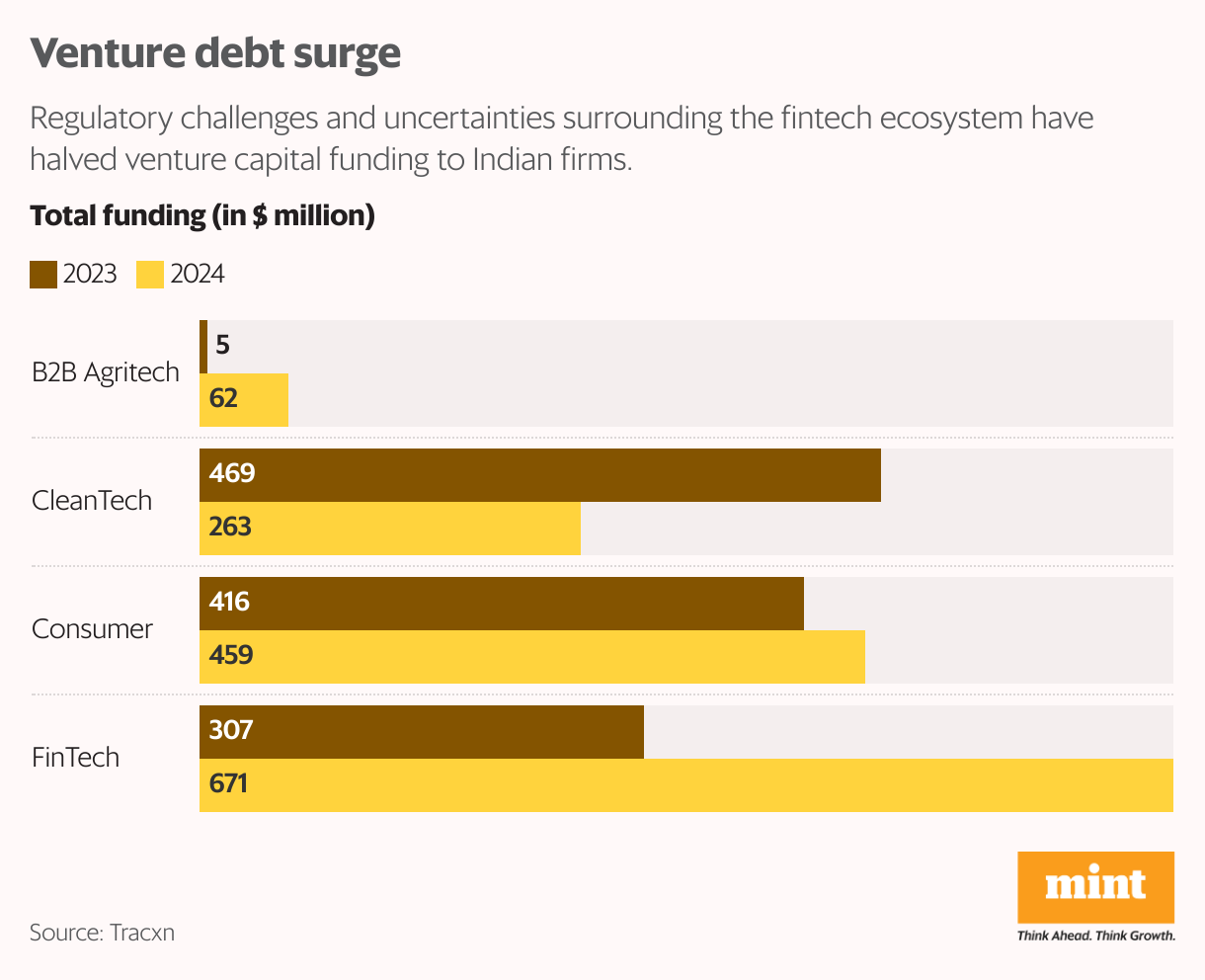

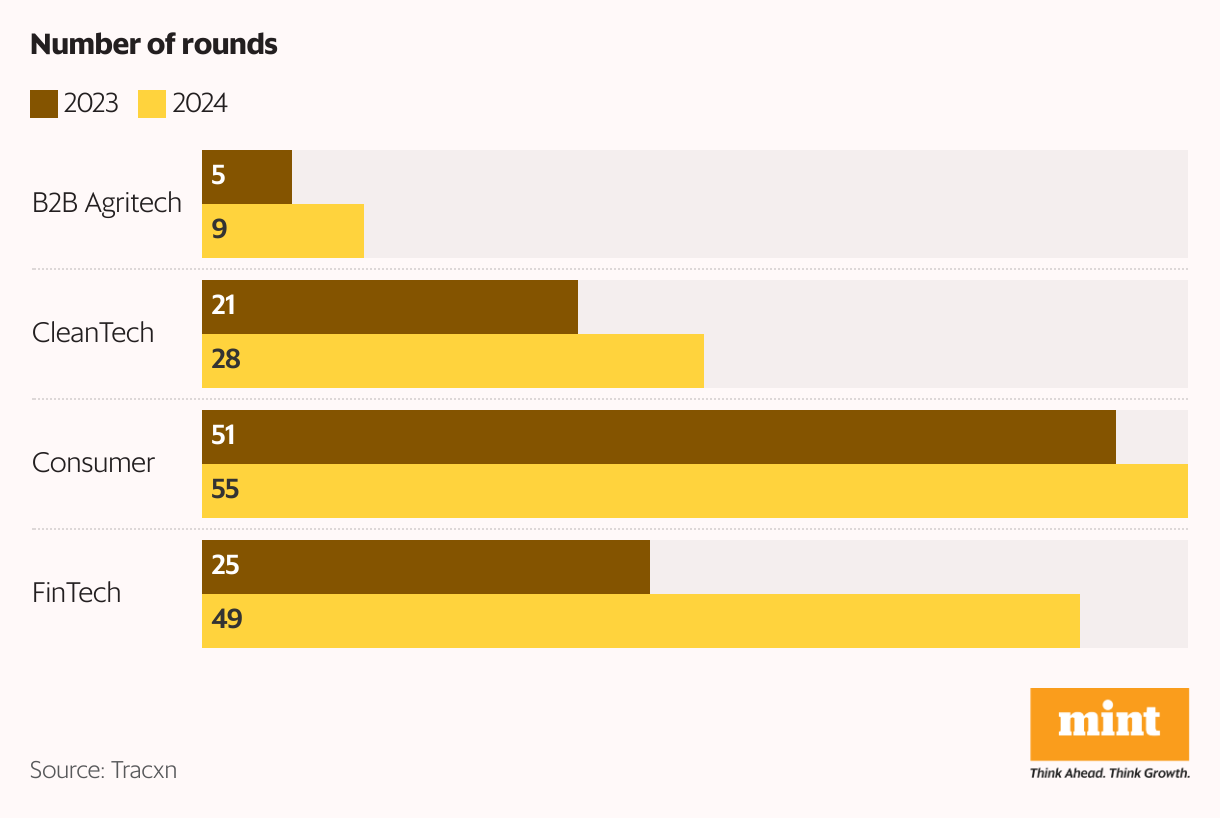

This year, fintech has emerged as the top sector for venture debt, with companies securing $671.1 million across 49 fundraising rounds, up from the $307.2 million they raised across 25 rounds in 2023, according to data from analytics firm Tracxn.

Regulatory sanctions and uncertainty in the fintech landscape have kept venture capital funds at bay, reducing equity funding to Indian fintech by almost half. Equity funding to India’s fintech sector in January-November dropped from $2.6 billion in 2023 to $1.6 billion in 2024, a decline of about 38% year-over-year, Tracxn data showed.

“Many of these (fintech) companies have scaled well, become profitable, and increased their retained earnings, which gives us comfort to lend to them, even as venture capital funding has slowed,” said Apoorva Sharma, managing partner at Stride Ventures, a venture debt firm.

Consumer startups followed, raising $459 million in venture debt across 55 rounds this year, marking a 10% growth from the $416.4 million of venture debt they raised in 2023.

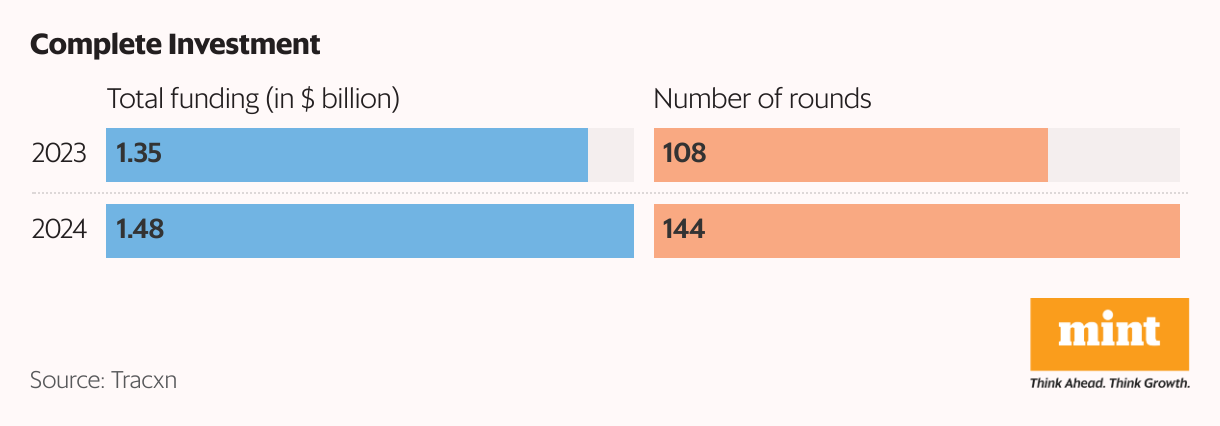

Total venture debt funding in India is up 10% so far in 2024 at $1.48 billion (it was $1.35 billion in 2023). This was driven not only by demand for non-dilutive financing but also as equity investors and startup founders continue to disagree on the lofty valuations that had been decided on during the startup boom of 2021.

The mainstreaming of venture debt

Venture debt is becoming mainstream for businesses across stages—from early-stage fundraising to pre-IPO, said Ankur Bansal, co-founder and director of BlackSoil Group, an alternative credit platform.

“It’s becoming strategic from a capital-efficiency perspective, from avoiding dilution, and for maintaining fiscal prudence at the business level,” Bansal said, adding thatin 2024there has been a 15-20% year-on-year increase in demand from startups for venture debt.

As per Tracxn data, venture debt funding rounds increased 33% to 144 in 2024 from 108 in 2023. This has come on the back of continuing optimism in alternative startup funding sources as equity funding for emerging companies, apart from sector leaders, continues to be scarce.

“There is a ‘missing middle’ primarily because VC activity in Series B to Series D rounds has been more muted,” said Sharma of Stride Ventures. Series B equity financing is typically raised by startups that are well-established but yet to reach their next phase of growth, while Series D financing is meant for more advanced companies.

Also read | India’s venture capital firms are finding that leaner might be better

Sharma said credit flows by venture debt funds this year were directly linked to overall venture capital activity in early-stage financing rounds having smaller ticket sizes or in later-stage, IPO-bound companies. This year has seen a revival in late-stage funding, which is likely to continue in the near term as more marquee companies prepare to go public, Mint reported earlier this month.

Stride Ventures—which has backed startups including electric scooter maker Ather Energy, construction materials marketplace Infra.Market, trading platform Upstox, and online pharmacy PharmEasy—earlier this month launched its fourth fund with a target corpus of $300 million, its largest yet. Sharma said the firm plans to allocate 10-15% of the corpus for profitable startups that aren’t backed by venture capital or private equity firms.

Apart from Stride, venture debt firms Alteria Capital and Trifecta Capital have also raised funds this year. In March, Mumbai-headquartered Alteria announced the final close of its third fund at ₹1,550 crore, while Trifecta launched its largest ever venture debt fund with a corpus size of ₹2,000 crore in August.

Also read | Trifecta launches its largest-ever venture debt fund at ₹2,000 crore

Changing sector picks

While venture debt firms continued to favour sectors such as fintech and consumer startups in 2024, cleantech, once a prominent segment for such funds, faced challenges this year, reflecting a strategic recalibration across the landscape.

Venture debt funding to cleantech declined by 44%, dropping from $468.6 million in 2023 to $263.4 million this year, though the number of financing rounds rose slightly to 28, signalling shrinking cheque sizes to the sector.

The business-to-business agritech sector registered a significant jump, raising $61.6 million in venture debt across nine rounds in 2024, compared to just $5.3 million over five rounds last year. It, however, remains among the least funded sector in terms of venture debt.

“We have maintained a calculated view on agritech. Despite a largeGMV (gross merchandise value), margins remain very thin, little value addition, and minimal technology integration are some of the issues with agritech,” said Bansal of BlackSoil.

A substantial amount of capital had been deployed to the agriculture sector in recent years, but it hasn’t delivered the best return on investment yet, he said.

Also read | VC firms turn cautious over AI startup hype

Leave a Reply